Quick answer: DBS, UOB and CIMB keep their rates tight for salaried Singaporeans who just want a clean, no-fuss application. Maybank and Standard Chartered throw in solid welcome gifts that can make a bigger loan feel less painful. Citibank gets cash to existing customers almost instantly. And if you would rather someone else do the legwork, Moneysmart lays the whole market out side by side so you know you are not missing a better deal.

Talking about personal loans can feel like admitting something went wrong. But here’s the quiet local truth: many of us use them for weddings, renovations, or just to smooth out cash flow. This is not about judgement. It’s a straightforward look at what actually matters—speed, flexibility, and the small-print things that affect your repayments—so you can agak agak which loan fits your life.

Part of Best Loans & Financing in Singapore: 12 guides covering this ground, for the wider view before you choose.

Taking a personal loan is one of those grown-up moves that nobody teaches you about until you are staring at a wedding deposit or a reno quote that is way more than you saved. The right loan is simply the one where the numbers work and the process does not make you want to throw your phone. These seven names keep popping up for good reason, and the choice really comes down to what you earn, how fast you need the cash, and whether a little perk sweetens things for you.

Moneysmart Singapore

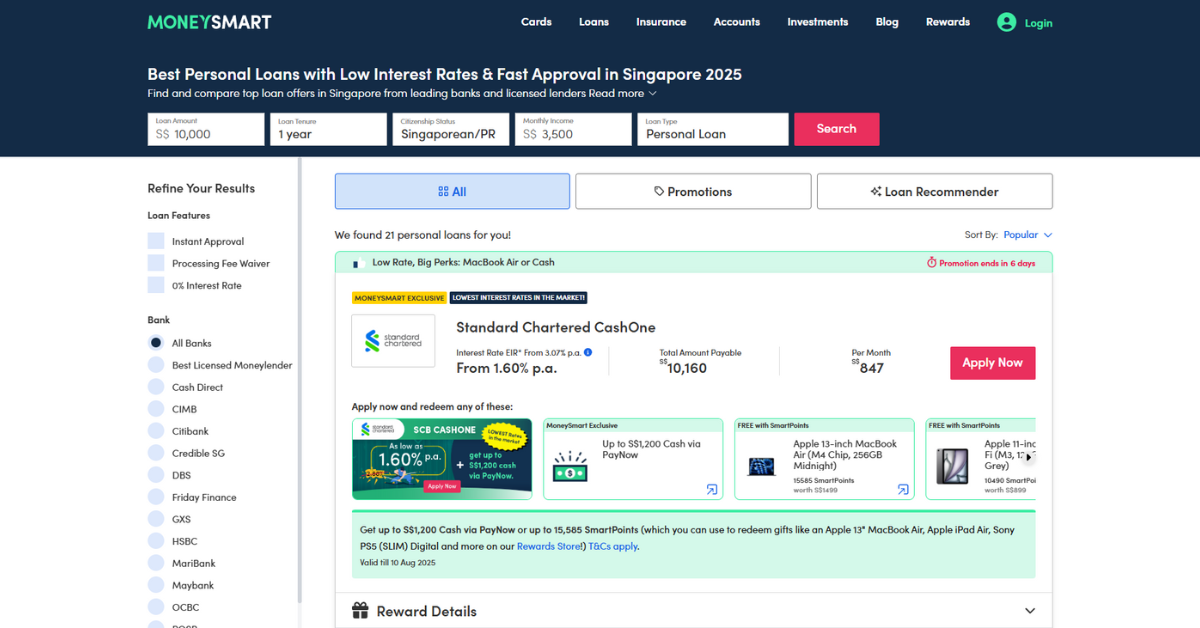

Not a lender itself, but a fintech platform operating out of Commonwealth that spares you the tab-hopping. You fill in one form and the system lights up with personal loan options from Standard Chartered, HSBC, UOB, Citibank and others—interest rates anywhere from 0% to 27.24% p.a., tenures from one to seven years, processing fees from S$0 to S$1,000. The site also flags exclusive promotions, like cashback up to S$1,700 or Apple goodies, so you are seeing what is actually on promotion, not just the sticker rate. Educational tools and loan calculators sit right there if you need to run the numbers before committing.

Many Singaporeans reach for Moneysmart when they are still shopping around and do not want to commit to a single bank’s chat funnel. It is especially useful if your income is ordinary or your credit profile makes you unsure which bank would even say yes—just key in your details and let the algorithm do the filtering. The interface is clean enough that even your uncle who still prints out his emails can manage.

When you prefer to scrutinise every available option before taking the plunge, Moneysmart is the perfect companion. One form, instant visibility across multiple banks—no need to field awkward calls from relationship managers. It’s perfect when you want to suss out the market quietly, maybe over a kopi on a Sunday afternoon.

Address: 8 Commonwealth Lane #04-02, Singapore 149555

Operating Hours: Monday to Friday, 10 AM – 7 PM

Contact: Via the contact form on their website

Website: moneysmart.sg/personal-loan

Maybank Singapore

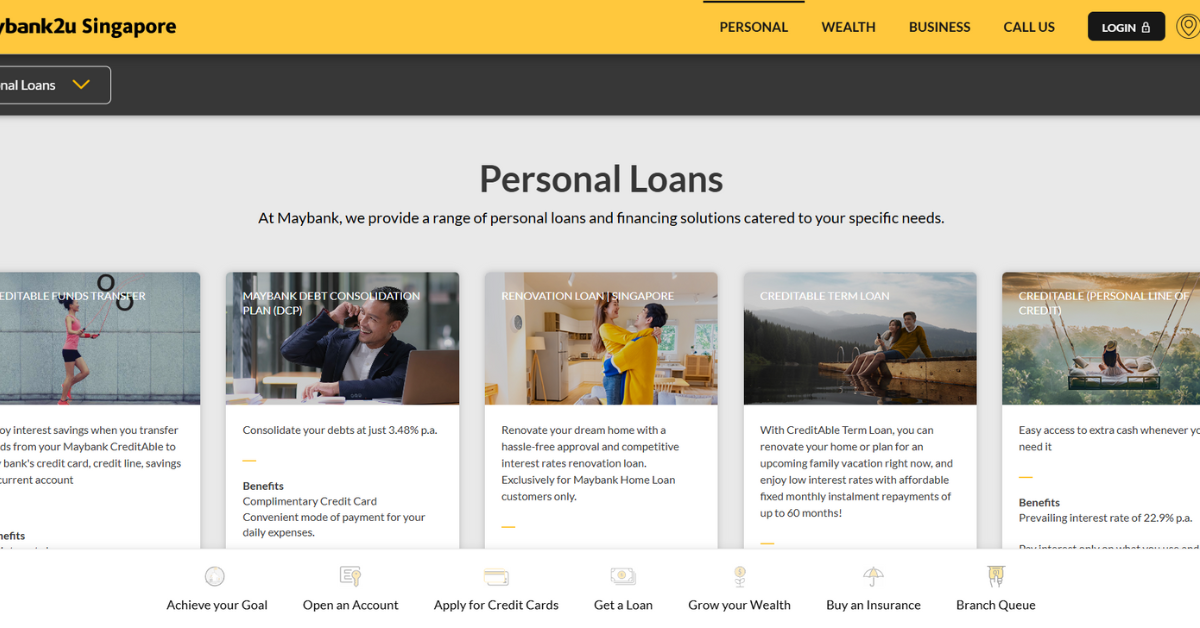

From their tower at 2 Battery Road, Maybank runs the CreditAble Term Loan with rates starting at 2.68% p.a. for online applications—sub-3% is honestly not easy to find unless you are an existing priority customer somewhere else. Tenures stretch up to 60 months, which gives you breathing room if you are spreading out a renovation or a long-haul holiday. Promotions run throughout the year, and at the time of writing they were giving out Apple AirPods for loans of S$10,000 and above—small thing, but if you were already planning to borrow that amount, it is a nice bonus.

The online application route saves you a trip to the branch. Their digital banking chops mean you are not filling in PDFs from 2007 or waiting three working days for someone to call you back. The minimum annual income is S$30,000 for Singaporeans and PRs, which puts this squarely in reach for most working adults who have been at their job a couple of years.

Maybank’s CreditAble Term Loan is quietly attractive for those who don’t have a priority banking relationship elsewhere. The online application rate dips below 3%—a figure that usually requires some inside track. It suits the planner who wants a straightforward, no-fuss repayment over five years and doesn’t want to keep checking for promos.

Address: 2 Battery Road, Maybank Tower, Singapore 049907

Operating Hours: Monday to Friday, 10 AM – 6:30 PM; closed on weekends and public holidays

Contact: 1800 629 2265

Website: maybank2u.com.sg

We choose these ourselves. If your place deserves a look for the next update, let us know.

DBS Bank

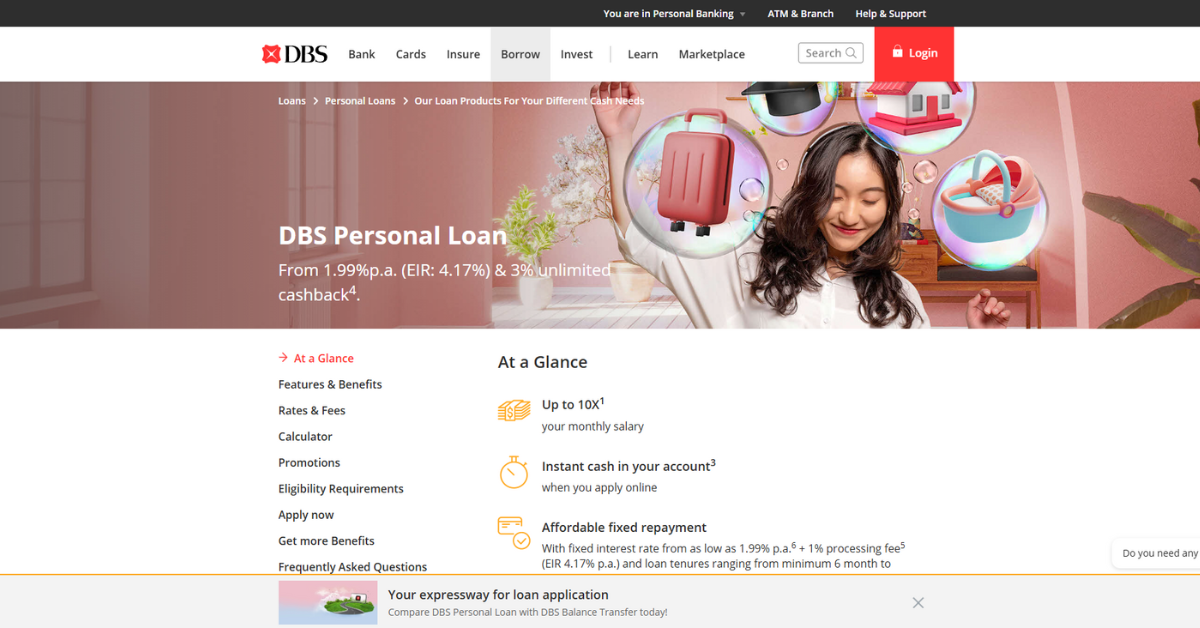

For many Singaporeans, DBS is basically the default—the app is already on your phone, your salary probably lands there, and the branch hours at places like Ang Mo Kio Ave 6 are long enough that you can nip in before work on a Saturday. Their personal loan lets you borrow up to 10 times your monthly salary if your annual income is S$120,000 and above; for incomes between S$20,000 and S$120,000, it is capped at 4 times. Rates start at 1.99% p.a. (EIR from 4.17% p.a. over five years), though if your income is on the lower end, the rate can go up to 11.00% p.a. with an EIR of 20.01% p.a.—which is brutally honest, and knowing it upfront helps you decide if you are better off exploring Money Lenders in Singapore for a smaller amount. They also have a separate Renovation Loan at 5.68% p.a. (EIR 6.40% p.a.) if you are specifically hacking walls and rewiring.

The approval speed is what people talk about, especially for existing DBS customers. The fee structure is laid out without drama, and the digibank platform means you can track everything from your phone while queuing for cai png. If you already do your banking with them, this is the path of least resistance.

If your salary already lands in DBS, this is the path of least resistance. The branch at Ang Mo Kio is open on Saturdays, so you can sort out a loan before brunch at a nearby kopitiam. The loan amount scales with your income, which makes sense for someone earning enough to borrow comfortably—it feels less like a gamble and more like a planned extension.

Address: 712A Ang Mo Kio Ave 6, #01-4066, Singapore 561712

Operating Hours: Monday to Friday, 8:30 AM – 4 PM; Saturday, 8:30 AM – 12:30 PM

Contact: 1800 111 1111

Website: dbs.com.sg/personal-loans

Standard Chartered Bank (Singapore)

Standard Chartered’s CashOne Personal Loan starts at 1.60% p.a., which works out to an EIR of 3.07% p.a. over five years—among the lowest effective rates you will see on this page. There is a S$199 first-year annual fee, but the overall cost can still undercut many competitors once you punch the numbers into a spreadsheet. Existing credit cardholders get access to the Credit Card Instalment Loan, which is useful if you are consolidating card debt into a single predictable payment. The minimum income is S$30,000 annually for Singaporeans and PRs.

Their Marina Bay Financial Centre office handles the paperwork, but the real action is online. Expatriates often gravitate here because the bank’s global network makes cross-border money management less of a headache, whether you are sending funds home or dealing with an overseas property. If you are holding a relatively high income and want the lowest headline rate with a clean, no-nonsense application, this is a strong contender.

Standard Chartered’s CashOne loan stands out for anyone who really sits down with a spreadsheet to compare effective interest rates. The effective rate is among the lowest you’ll find, even after the modest annual fee. It’s the sort of loan that rewards a bit of calculation—perfect if you don’t mind a small upfront cost for long-term savings.

Address: Marina Bay Financial Centre, Tower 1, 8 Marina Blvd, #01-01, Singapore 018981

Operating Hours: Monday to Friday, 10 AM – 5 PM

Contact: +65 6747 7000

Website: sc.com/sg/cashone

We choose these ourselves. If your place deserves a look for the next update, let us know.

United Overseas Bank (UOB)

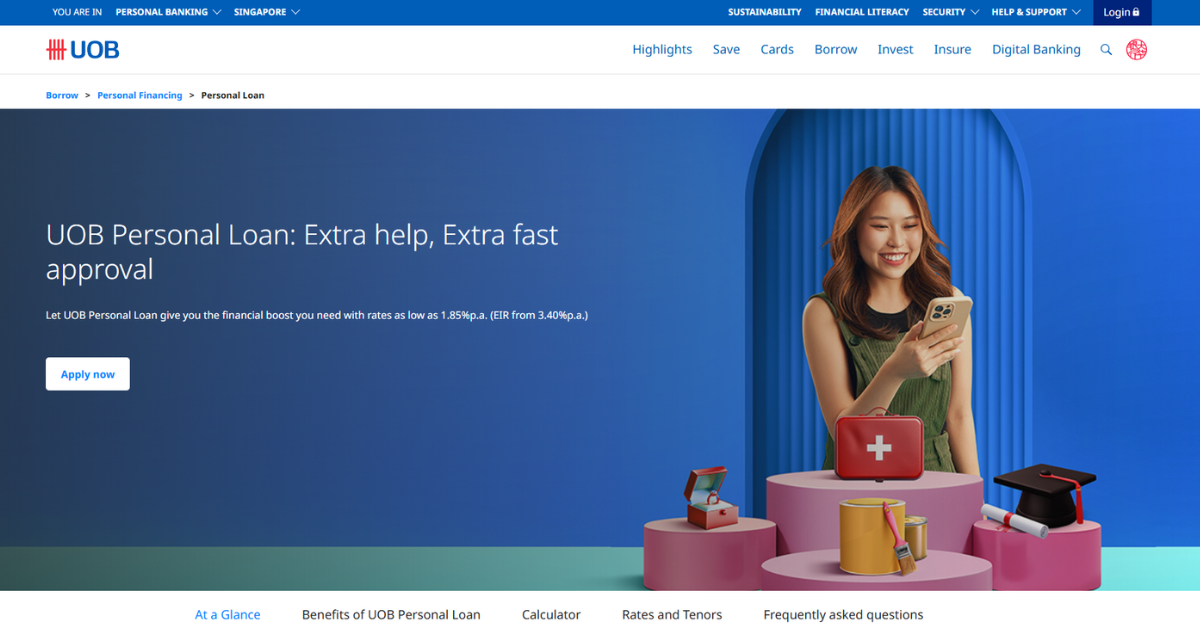

UOB’s personal loan sits at 1.85% p.a. with an EIR from 3.40% p.a., and the deal gets more attractive if you are borrowing S$15,000 or more over three to five years—they hand back up to 2% as a cash rebate. That rebate can cover your first couple of months’ interest, which feels like a small victory when you are already writing a large cheque for a wedding banquet or a contractor. The JEM branch at Jurong Gateway is one of many across the island, so you are never far from a counter if you need face-to-face help.

Existing UOB customers tend to get the nod very quickly, and the digital tools make ongoing management less sian. The minimum income is S$30,000, and the tenure options of three to five years hit the sweet spot between keeping monthly payments manageable and not dragging the loan out so long that the interest piles up. If you are planning a milestone expense and want a tangible rebate that puts money back in your pocket, this is a practical pick.

There’s a small victory in UOB’s cash rebate when you’re already signing off on a big payment for a wedding or a contractor—the 2% return can cover your first month’s interest. The JEM branch in Jurong Gateway is a handy stop if you live out west, and the loan terms reward you for borrowing a bit more over a sensible period.

Address: 50 Jurong Gateway Road, #02-15 JEM, Singapore 608549

Operating Hours: Monday to Friday, 11 AM – 6 PM; Saturday, 11 AM – 4:30 PM

Contact: 1800 222 2121

Website: uob.com.sg/personal-loan

Citibank Singapore

Citibank’s Citi Quick Cash loan starts at 3.45% p.a. (EIR from 6.50% p.a.), which is not the lowest headline figure, but the hook is speed—existing customers can get approval and disbursement almost instantly, with no processing fees to eat into the amount you actually receive. They run promotions like S$200 cashback for loans of S$8,000 and above, which takes a little sting out of the higher rate. The minimum annual income is S$30,000 for Singaporeans and PRs.

This is the one to reach for when you cannot wait. Car breakdown, medical bill, a contractor who suddenly demands an upfront top-up—whatever the emergency, Citibank’s digital platform is built for speed, not paper-pushing. Their global reach also helps if you have commitments overseas that need settling in a different currency. It is not the cheapest way to borrow, but when time is money, the math still adds up.

When speed trumps everything, Citibank’s Quick Cash is the obvious go-to. Existing customers can see funds land almost instantly, with zero processing fees taken off the top. The headline rate is higher, but the no-fuss disbursement makes it a favourite for urgent situations—like a last-minute medical bill or a sudden travel need that can’t wait.

Address: Asia Square Tower 1, 8 Marina View, #21-00, Singapore 018960

Operating Hours: Monday to Friday, 9:30 AM – 6 PM

Contact: +65 6224 5757

Website: citibank.com.sg/loans

CIMB Bank

Operating out of Raffles Place, CIMB quietly offers some of the most competitive numbers around—rates from 1.86% p.a. (EIR from 3.56% p.a.) and loan amounts up to S$200,000, which is double what most banks cap at. That high ceiling makes it a genuine option for larger renovations, education fees, or consolidating multiple debts into one fixed payment. Disbursement via PayNow means the money hits your account as soon as the approval comes through, no waiting for a cheque or a batch transfer window.

The digital-first approach means you apply from your couch and skip the branch visit entirely. The minimum income of S$20,000 for Singaporeans and PRs is the lowest on this list alongside DBS, so younger earners or those just past the probation period can still qualify. If you are disciplined about repayments and want the combination of a low rate and a high borrowing limit, CIMB is tough to beat. Once the loan is settled, you might even have headspace to think about Fixed Rate Home Loans in Singapore further down the line, or simply get a grip on daily spending with one of the Savings Tracker Apps in Singapore for Financial Mastery.

CIMB’s personal loan is the quiet giant if you need a serious amount—up to S$200,000, which is about double the usual limit. That makes it genuinely useful for a full-scale renovation or consolidating multiple debts into one fixed monthly payment. The PayNow disbursement is seamless, so once approved, the money hits your account like a regular transfer.

Address: 30 Raffles Place, #04-01, Singapore 048622

Operating Hours: Monday to Friday, 9 AM – 4:30 PM; Saturday, 9 AM – 1 PM

Contact: +65 6333 7777

Website: cimb.com.sg/personal-loan

How to choose

Start by being honest with yourself about why you are borrowing. A wedding or a renovation loan can be sensibly spread over three to five years without guilt—the interest cost is the price of keeping your savings intact. Consolidating credit card debt is a different animal: the interest rate matters even more because you are replacing high-cost debt, not taking on new spending. In that case, chase the lowest EIR you can get, not the flashiest promotion.

Income eligibility is the quickest filter. If you earn under S$30,000 annually, your realistic options are DBS, CIMB or going through Moneysmart to check who will take your profile. Above S$30,000, the field opens up and you can start comparing perks. Standard Chartered and CIMB tend to lead on low effective rates. Maybank and UOB are strong when you are already taking a decent loan quantum and want a tangible gift or rebate. Citibank is the emergency button—higher cost, near-instant access for existing cardholders.

For a five-year loan of S$20,000, you can reasonably expect an EIR between 3% and 7% from most banks here, depending on your income and credit score. Use the calculators on Moneysmart or the individual bank sites to see the total interest payable over the whole tenure, not just the monthly instalment. A 2.68% p.a. flat rate and a 1.99% p.a. flat rate sound close but can mean a few hundred dollars difference in your pocket by year five.

One last thing: a loan stretching longer than five years makes each month easier but adds serious interest cost. If you are tempted by seven-year tenures, run the total repayment figure first and ask yourself whether that extra year or two is worth it. In many cases, a tighter budget for a shorter period saves more than any cashback offer.

Comparison at a glance

| Provider | Interest Rate (p.a.) | EIR (p.a.) | Loan Tenure | Min. Income (SG/PR) | Key Features |

|---|---|---|---|---|---|

| Moneysmart Singapore | 0%–27.24% | Varies | 1–7 years | Varies | Comparison platform, cashback up to S$1,700 |

| Maybank Singapore | From 2.68% | Not specified | Up to 60 months | S$30,000 | Apple AirPods for S$10,000+ loans |

| DBS Bank | From 1.99% | 4.17%–20.01% | 6–60 months | S$20,000 | Up to 10x monthly salary, renovation loan |

| Standard Chartered | From 1.60% | 3.07%+ | Up to 5 years | S$30,000 | CashOne loan, credit card instalment option |

| UOB | From 1.85% | 3.40%+ | 3–5 years | S$30,000 | 2% cash rebate for S$15,000+ loans |

| Citibank Singapore | From 3.45% | 6.50%+ | 1–5 years | S$30,000 | No processing fees, S$200 cashback |

| CIMB Bank | From 1.86% | 3.56%+ | Varies | S$20,000 | Up to S$200,000, instant PayNow disbursement |

Summary

A personal loan is just a tool—the numbers either work for your situation or they do not. Moneysmart gives you the widest view, while the six banks each have a clear strength: rock-bottom effective rates at Standard Chartered and CIMB, high borrowing limits at DBS and CIMB, instant cash at Citibank, and rebates that feel like a small win at Maybank and UOB. Pick the one whose terms fit your income and your timeline, and read the EIR more carefully than the flashy headline rate.

We choose these ourselves. If your place deserves a look for the next update, let us know.

Disclaimer: Interest rates, fees, promotions and eligibility criteria can change. Confirm the latest terms directly with the provider before applying. Nothing here is financial advice—speak to a qualified adviser if you are unsure about your borrowing capacity.

Frequently asked questions

What is the difference between the advertised interest rate and EIR?

The advertised rate is usually a flat rate applied to the principal. The Effective Interest Rate (EIR) accounts for compounding, processing fees and the reducing loan balance over time, so it gives you the true annual cost. Always compare EIRs across banks, not the headline flat rate.

Can I get a personal loan if I earn less than S$30,000 a year?

Yes, both DBS and CIMB accept a minimum annual income of S$20,000 for Singaporeans and PRs. Moneysmart also lets you filter by income so you can see which lenders will take your profile at a glance.

Which bank gives the fastest approval?

Citibank and CIMB both highlight instant approval and fast disbursement for existing customers, with CIMB using PayNow to get funds into your account immediately. DBS and UOB are also known for quick turnaround if you already bank with them.

Are there any promotions worth looking out for?

Several banks run ongoing promotions. Maybank offers Apple AirPods for loans of S$10,000 and above. UOB gives up to 2% cash rebate on S$15,000 and above over three to five years. Moneysmart aggregates these promos so you can see what is active when you apply.

Can expatriates apply for these loans?

Yes, but eligibility depends on your residency status and income level. Banks like Standard Chartered and Citibank are often more familiar with expatriate profiles and cross-border financial needs, but you will need to check the specific income and employment pass requirements with each bank.

Should I use Moneysmart or go straight to the bank?

Moneysmart saves time if you want to compare multiple banks in one place and spot the best promotion. Going directly to the bank works well if you already know which one you want, especially if you are an existing customer and can benefit from faster approval.